How Credit Card Interest Works

- Strike Force Agency LLC

- Oct 3

- 2 min read

Credit cards are powerful tools — but if you don’t understand how interest works, they can quickly turn into a financial trap. APR, grace periods, and compounding daily charges aren’t just fine print — they’re how banks profit.

At Strike Force Agency LLC, we’ll show you how interest really works — and how to beat the system.

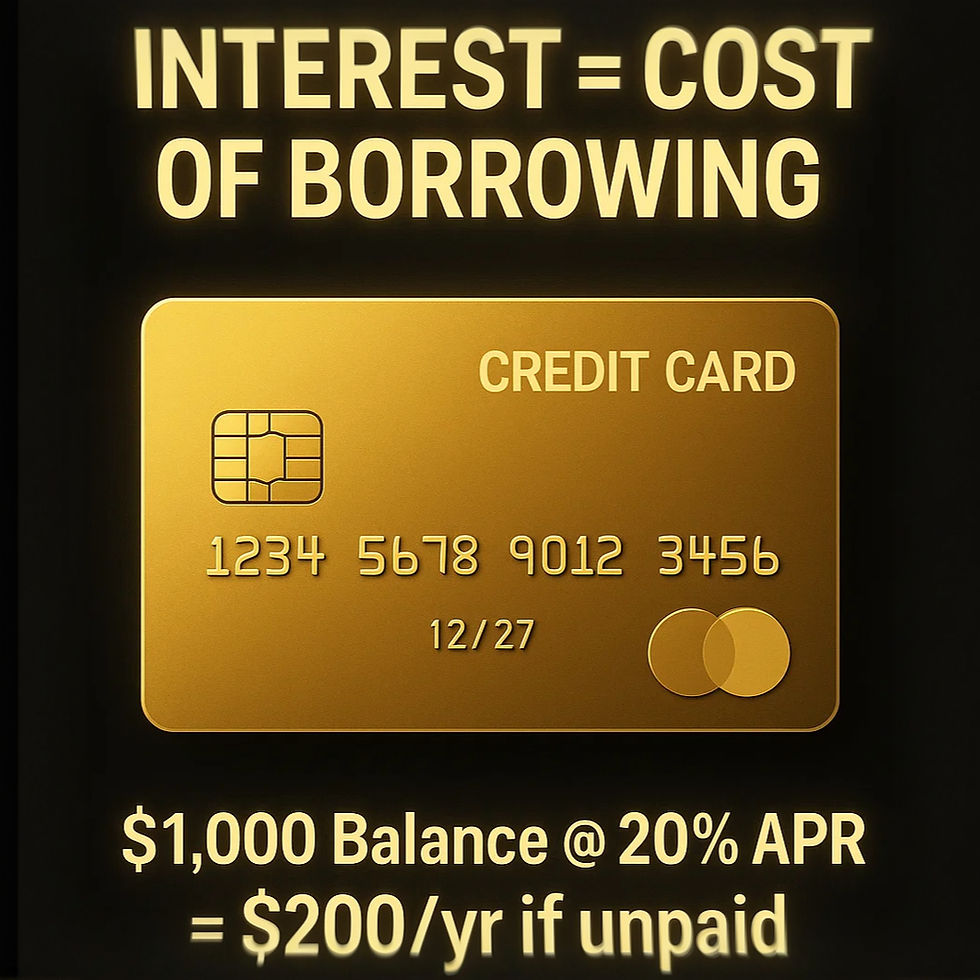

What is Credit Card Interest?

Credit card interest is the cost of borrowing money. It’s charged when you carry a balance past your grace period.

Example:

Balance: $1,000

APR: 20%

Carrying that balance could cost you $200+ a year in interest.

How APR Really Works

APR varies depending on the type of transaction:

Purchase APR

Cash Advance APR

Penalty APR

Introductory APR

The Grace Period Advantage

Most cards give you 21–25 days interest-free if you pay in full. Carry even $1 forward, and interest applies to the entire balance.

How Interest is Calculated Daily

Formula: Daily Balance × (APR ÷ 365) = Daily Interest Charge

Example: $1,000 × 20% ÷ 365 = $0.55/day. That’s $16.50/month.

Why Minimum Payments Are Dangerous

Paying minimums keeps account current, but barely reduces principal.

Example: $1,000 @ 20% APR, $25 min → 5+ years payoff + $600+ interest.

Strike Force Expert Tip

Pay in full if possible.

Keep utilization <30% (10% if preparing for funding).

Rotate spending across cards.

The Bottom Line

Credit card interest is predictable once you understand it. Banks want you confused — Strike Force makes you informed.

⚡ Want to stop paying banks extra? Get educated, fix your credit, and put yourself in a position for high-limit approvals.

👉 Book your free consultation today.

👉 Download your FREE Credit Dispute Kit and start taking control:

Start your own Credit Repair Journey with our Free Dispute Starter Kit.

Comments